By Huang Zixun

It is often said that the biggest fear that keeps people from investing is the fear of losing their hard-earned money. This is understandable as the certainty of cold, hard cash in hand definitely beats the uncertainty of investments. Furthermore, horror stories of other investors’ savings wiped out by events such as Noble Group’s share price collapse and Hyflux’s insolvency have certainly not helped matters.

In view of that, diversification acts as a defensive investment strategy to lessen losses. So what exactly is diversification? In layman terms, it is all about “not putting your eggs in one basket”. This means that investors actively allocate their capital in a manner that reduces any exposure to any one particular asset or industry. Hence, even though no asset is truly risk-free, diversification mitigates risk across the entire portfolio.

Types of Risks, Asset Allocation and Diversification

Before going into diversification proper, it would be best to give a general overview of the two main types of risks associated with investments. This would clear up some misconceptions associated with asset allocation, diversification and the risks that they reduce.

1. Unsystematic Risk

This form of risk commonly occurs within a specific company or industry. While this form of risk typically occurs due to internal factors within the organisation, industry-wide events can negatively impact share prices by exposing business risk.

Graph of Keppel Corp’s share price in relation to oil prices. Source: BP Wealth Learning Centre

To illustrate this, as seen in the graph above, Keppel Corp’s share value was more than halved between 2014-2015. This was due to a crash in oil prices, and the same was also true across the offshore and marine industry. If prior to 2014, an investor’s portfolio comprised only of stocks from that industry, the portfolio’s value would have suffered a massive decline.

However, suppose the portfolio had increased diversification. An example would be concurrent holdings in the airline or transportation industry which by and large, benefitted from lower oil prices due to cost reductions. Gains in those areas would have reduced any losses incurred from holdings in merely the offshore and marine industry.

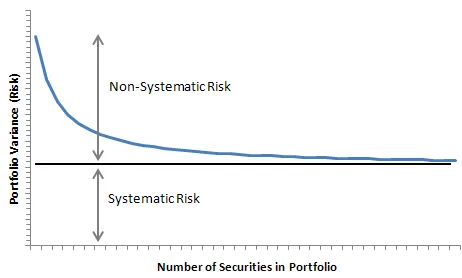

Risk and Diversification. Source: ValueWalk

2. Systematic Risk

Also known as market risk, such risks are commonly associated with macro factors, typically caused by changes occurring across the entire market such as interest rate changes or economic recessions. It is highly unpredictable and impossible to avoid as the entire market is affected by these broad events. Systematic risk is not diversifiable as the value of financial instruments across the market are affected. This means that simply increasing the types of shares held, if your portfolio is already well diversified, will not aid in reducing systematic risk.

With this in mind, a common method used to reduce systematic risk is through careful asset allocation. Contrary to popular belief, asset allocation is different from diversification. An investor whose portfolio consists entirely of 50 equities across multiple industries has good diversification. However, that is an example of poor asset allocation, and the value of that portfolio would plummet in the event of a stock market crash such as the great recession in 2008, which is an example of systematic risk.

Thus, a balanced asset allocation with the inclusion of components such as fixed income and interim cash would act as a hedge against such risks. In order to effectively mitigate risks, asset allocation should be utilised in conjunction with diversification.

Cost-effective Methods for Diversification

One of the main drawbacks of diversification is the potential high cost involved. Not everyone will have the capital to purchase more than 20 different equities. Thus, here are 3 cost-effective components to consider adding to your portfolio to improve asset allocation and diversification.

1. Exchange Traded Funds (ETFs)

ETFs are a form of investment funds that hold a group of assets such as stocks or bonds, and are listed and traded on the stock exchange. One prominent example in the Singapore market is the Nikko AM Singapore STI ETF that tracks all 30 companies in the Straits Times Index which has generated a 9.54% annualised return since its inception in 2009. Other than stocks, other prominent ETFs in the SIngapore market include the Lion Philip S-REIT ETF that tracks Real Estate Investment Trusts (REITs) in Singapore, as well as the ABF Singapore Bond Index Fund that holds investment-grade bonds.

Among retail investors, ETFs are one of the most popular forms of investments nowadays, for a good reason. Primarily, ETFs provide a simple and low cost way to diversify a portfolio by exposing investors to a range of asset classes across multiple industries. Furthermore, ETFs have much lower management fees of less than 1% as compared to unit trusts or mutual funds that have management fees of up to 5%.

2. Fixed Income

Bonds have traditionally been overlooked by many retail investors (at least for investment-grade bonds) because their potential returns are not as high as equities due to the lower risk involved. However, volatility in the global markets have led to many investors diversifying their equity-heavy portfolio to guard against a bear market. In fact, during the 2008 recession, while US equities fell by 45%, the treasury bond market benefited, as 10-year US treasury bond yields fell from 3.91% to 2.89. This meant that treasury bond investors made a profit, and investors who held a mixture of bonds and equities would have suffered a much smaller loss than those who had a pure-equity portfolio.

In the Singapore context, Singapore Savings Bonds have been seen by retail investors in recent years as a viable fixed income asset backed by the Singapore government. However, over the past year, average yields have been steadily falling. Alternatively, bond funds such as the ABF Singapore Bond Index Fund, as well as the Nikko AM SGD Investment Grade Corporate Bond ETF, are also effective methods of diversification as those funds invest in a basket of bonds.

3. Robo-advisors

A relatively new development on the market, robo-advisors refer to online investment platforms that perform investment management with minimal human intervention. Their differentiating factor from other funds would be their lower expense ratio as compared to traditional fund managers due to the fewer man-hours needed to manage the fund. Usage of such services are ideal for investors who are more hands-off and are looking for a more simplified and convenient investing process. Custom portfolio asset allocation can also be structured as they weigh expected returns against risk appetite. Furthermore, diversification can be achieved as robo-advisors would invest in a mix of equities and fixed income assets across regional and even global markets. Prominent robo-advisors based in Singapore include DBS digiPortfolio and StashAway.

To Conclude

Overall, diversification as an investment strategy is a viable method for risk reduction. However, one must bear in mind some of the drawbacks as well. The basic rule of investments still apply: with lower risks, comes lower returns. As diversification reduces large potential losses by averaging out risk and volatility, it equally reduces large potential gains. Thus, if you have a high risk appetite and the financial know-how, a concentration strategy may be a better fit for you.

Furthermore, it is worth reiterating that pure diversification will not protect against market-wide systematic risk, because in recessions, the entire market will go down regardless of industry. To mitigate such risks, careful asset allocation has to be implemented in tandem with diversification. For best results, due diligence has to be done before making any form of investment to ensure sufficient knowledge of the risk level and how it would value-add to your portfolio.

References:

Why diversification matters – https://www.fidelity.com/learning-center/investment-products/mutual-funds/diversification

Why it’s important to diversify your investments and how to go about doing it – https://www.todayonline.com/singapore/why-its-important-diversify-your-investments-and-how-go-about-doing-it

Keppel share price with oil crash – https://bpwlc.com.sg/keppel-corp-sembcorp-marine/

Unsystematic vs Systematic Risk – https://www.blackwellglobal.com/unsystematic-vs-systematic-risk/

Managing (systematic) risk – http://www.sr-sv.com/managing-risk/

Risk & Diversification Graph – https://www.valuewalk.com/2016/03/warren-buffett-thinks-risk-2/

Art of diversification – https://dollarsandsense.sg/the-art-of-diversification-what-you-should-know-if-you-want-to-diversify-your-investment-portfolio-effectively/

ETFs Overview Singapore – https://blog.moneysmart.sg/invest/index-fund-etf-singapore/

Nikko AM STI ETF – https://www.nikkoam.com.sg/etf/sti

Bonds in a bear market – https://www.thebalance.com/what-happens-to-bonds-in-a-stock-bear-market-417053

Robo-advisors for diversification – https://www.thebalance.com/what-is-a-robo-advisor-and-how-do-they-work-4097134

Why robo-advisors – https://www.drwealth.com/why-use-robo-advisors-at-all/